Who Is The Best Financial Expat Advisor?

The best financial expat advisor is one who looks at your situation, understands the problems, and is able to give you an effective solution. The are plenty of expat advisors out there who want the commission from transferring a pension or putting your money in poor-performing funds because they pay the most commission!

When it comes to the best expat financial advisor, it is probably someone who can pick good investments, has a good record with their clients, and charges a reasonable fee for a service. In order to understand my strengths and see if I am the best financial expat advisor for you, here are the ways I pick funds, stocks, and create portfolios and what I am best known for.

How to create a portfolio

I have been asked lots of times is “how to pick and create a portfolio”. This is subjective to your age, time, and investment horizon. When working on portfolios I usually go for a textbook approach depending on your time frame for the investment horizon and risk profile. The definition of what stocks and shares you should have depends on your risk levels and do differ on each side of the Atlantic in percentage amount of international equity and alternative investments. We will keep it simple and generalize with both the American and European models.

Level of risk you can take?

First, you need to ask yourself, what is your risk profile?

This will mainly be down to how long you are looking to invest, how much you can risk losing & what your aspirations are as well as your investment knowledge and experience. Use the link below to find out your risk profile, it’s good to do this for most investments.

https://www.surveymonkey.com/r/SB36VNM

This will put you into set levels or risk categories that are most applicable for you and use the models as guidelines. Although if you are doing this with a financial advisor or by yourself, you or the advisor should take deeper consideration about your personal situation & if you have a pension or own property or other investments.

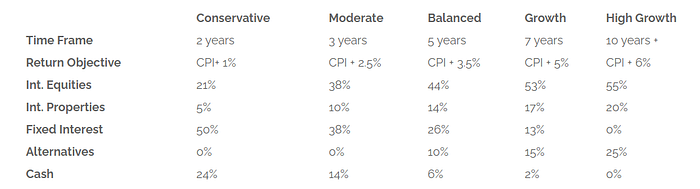

Conservative risk profile

If you have done the test and have a low-risk profile. This is normally for older personnel with pension funds that want something stable and looking for a medium-term investment (5–10 years). Here is an example of a conservative portfolio:

Table 1: Conservative risk profile, 70% allocation to fixed interest, 20% equity, and 10% cash money markets

As you see in the table (above) shows that this is where the majority of your money allocated to fixed income securities are mainly bonds, that give a general return and are lower risk than equity. With fixed income bonds, can be either corporate or government bonds with the latter being more conservative (mostly).

The typical investor in this portfolio would want to keep their money well persevered and get around 3–4% of growth per year average, this normally beats inflation in most developed countries (CPI stands at around 2% in most developed countries as of 2019) thus giving a net return of just over 2% in real terms. It’s not the most glamorous returns, however, if you have a sum of money and want to preserve the wealth and maintain it in the medium to long term with some growth, it is an appropriate option.

Here are some of the portfolios that have used previously for conservative investors:

*Note this is for GBP, it is not applicable for USD or EUR but is used as an indication and was a model portfolio that was previously designed for an individual for his/her personal circumstances so it will not be applicable to anyone else*

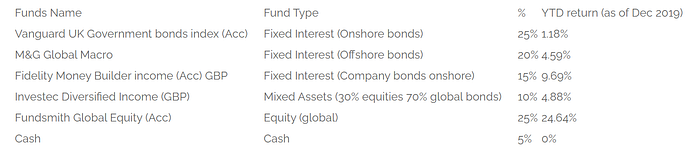

Table 2: Shows the funds used in the conservative portfolio

Shows the funds used in the conservative portfolio

As shown from the table, this was an example of a U.K client with money in GBP, as you can see it nearly fits the assets allocation for a conservative risk profile used in the chart above. I prefer to have less money devoted to cash as some of the equity and mixed assets classes will hold a proportion of their fund in cash (varying to what they expect from the market). As well as this it has several fixed interests across a number of asset classes thus giving an alternative to the home country’s government bonds with a range of European and American with a minority of developing countries, such as Brazil, Indonesia in the Investec bond. These normally give higher returns than the developed country-specific bonds. This is seen in the M&G global macro bond returns compared to the Fidelity U.K bond returns.

The equity in this particular portfolio is higher than that that has been advised, however, underline that for a risk-reward trade-off and the client was happy to do so. If you are looking after a pension fund or want something more stable you may consider putting more into fixed interest across a range of different sectors.

Aggressive portfolio

The aggressive risk is normally for someone who wants to get higher than average returns, this is looking more into the longer-term period and higher returns and can be used for a younger investor. This will take the ideology of looking for higher returns of around 6–8% per year & the asset allocation that I personally use (but does vary for each individual) is as follows.

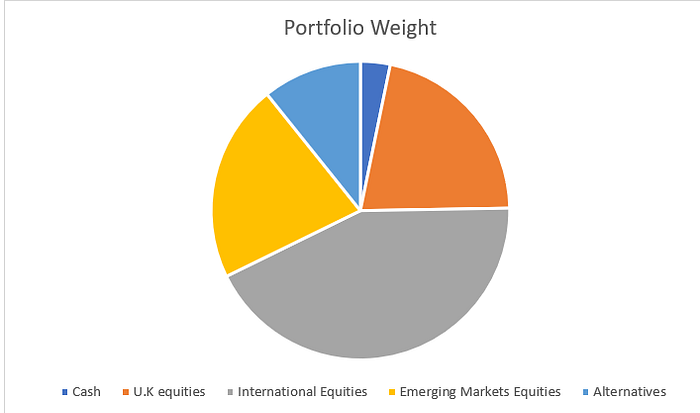

Table: Shows the allocation of an aggressive portfolio

As seen from the chart above, this has a majority in equities and I have taken it down into sub-sections on how the asset allocation has been distributed.

Again this is for a U.K client so therefore the majority of the assets that take place are done in global equities, this is done in mainly the U.S, Western Europe, and in large market capitalization companies. The same to a lesser degree of the U.K equities. With the emerging markets, this takes around 20% of the portfolio and gives access to the developing markets to give a higher growth than that of the developed indexes, this selection has a highly-rated Asian bond by JP Morgan giving access to developed large companies in Singapore and fast-growing countries in Indonesia, Thailand & Vietnam. This particular portfolio is on the aggressive end and was done for a specific need, however, if you wanted to make it less aggressive I would add more bonds and for the alternative, I would go into a gold ETF to give some diversification from equities.

Here is a GBP portfolio that was made from this, when selecting the funds I went for those with a high market capitalisation, made sure it was a major name and a 3+ star-rated for every fund by at least 2 independent rating agencies with the global equity looking 4/5 stars. I used Morningstar and S&P, but I do prefer Morningstar.

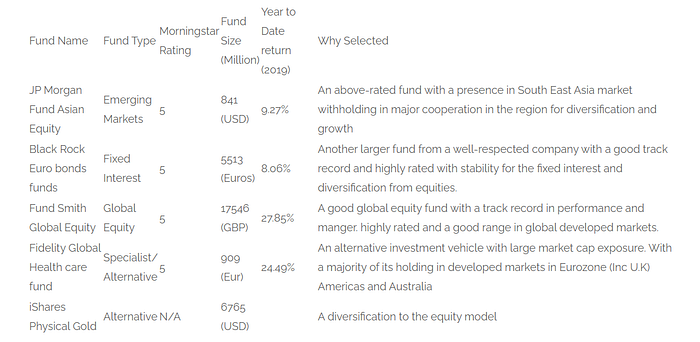

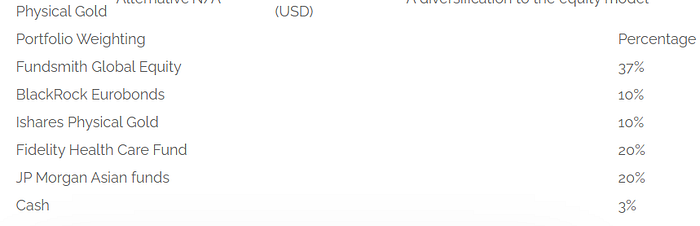

Table 4: Shows the rating and the fund type rating and size of the fund selected with the return to date.

Table 6 shows a pie chart of the weighting

Disclaimer

*Please note again that this is just an example of a portfolio and how we have selected for an induvial and the model based on personal aspirations and circumstances. This may not be applicable for you and would seek financial advice before making any decision on investing.*

How I benchmark my portfolios

This is the model I use when deciding how to create a portfolio on the basis of how long that you are wanting to invest and what your risk profile is.

I have written three example portfolios depending on the level of risk.

The first is a defensive model this is more suited for a stable pension fund investor and looking just past the level of inflation.

See that this model is more geared towards fixed interest than the volatility of equities.

Model Portfolios: Defensive

*Note that this is selected from a restricted fund choice but have equated enough portfolio to adequate a risk-averse portfolio

This is a defensive portfolio that has been selected with the funds available, not that it has an element of developed fixed assets around the developed world. With a small proportion of developing (Asian funds) as well as this it has an element of global Equity to assist with the growth of the fund, as well as property. All the funds selected are major funds in their selected and used the approach used above as well have used a tracker fund as still believe in having a tracker as a proportion of the portfolio.

Balanced Model Portfolio

Growth Portfolio

Key Words

- Gross Domestic Product (GDP) — the total value of goods produced and services provided in a country during one year. Compare with gross national product.

- Interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited or borrowed (called the principal sum).

- Inflation is a sustained increase in the general price level of goods and services in an economy over a period of time.

- Growth at a Reasonable Price (GARP) is an equity investment strategy that seeks to combine tenets of both growth investing and value investing to select individual stocks.

- The price/earnings-to-growth (PEG) ratio is a company’s stock price to earnings ratio divided by the growth rate

The Funds and Platforms

The platforms, if in the offshore bonds such as RL360 or FPI can be expensive and offer a commission to the advisor, so ensure you are going into them for the right reasons and not just to pay the advisor. The funds, if you want to be sure, make sure they are listed on HL SIPPs platform, this will ensure that at least they are available in the U.K. If you want to double-check go to Morningstar or Trustnet for a non-bias rating agency. I would stay clear of low-risk profiles or anything that is below 3 stars. Do your research before you are invested in any funds.

The reality is if you are sticking with solid funds you will most likely never have to use any of these protection schemes.

How do U.K options compare to offshore investments?

I have written a number of articles on offshore options and U.K options. The ISA options in the U.K. are pretty competitive. Here is a summary of some of the most used U.K platforms.

- Note with the fund management charges are based on an average, some funds such as ethical investing will charge more.

- A.J bell does reduce their fees for accounts over 250,000–1 Million

Analysis of these platforms in the U.K has done well in getting competitive fees with platforms. If you are looking for DIY platforms these are not bad options.

For managed funds, it is harder to gauge fees, the FT did an article on this with experienced financial professionals spending hours looking for fees for managed platforms the average was 1.2% with advisor fees and initial charges of 1%. This should be in the average for advisor fees

The FT has done an article on the Fees of SIPPs and I have included the link below.

Robo vs Actively managed funds

I have had a Nutmeg account and have come on some other Robo-advisors Wisdom tree. I believe for the novice investors these are great in theory, the problem I have is that they just don’t perform. I had a Nutmeg at level 10 risk to try it out, its overall performance over that time was 2% (not a loss). My other funds and portfolio were up 22% over the same time frame (mostly in global large-cap equities). I have also spoken to friends that have money invested at a lower level that has had less. It hasn’t been negative but is far behind a good portfolio. This can be the same for other Robo advisors, they have failed to live up to their fund portfolio.

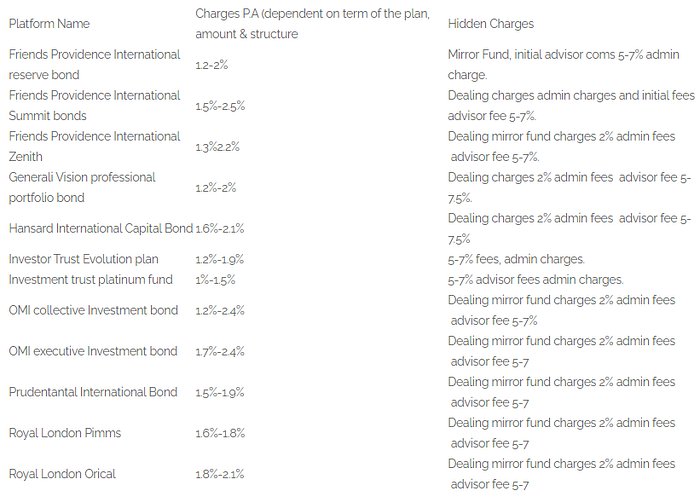

Offshore platforms

At a glance, tax-efficient saving seems a good option and I would agree as I will cover the tax saving options later. However, the platforms I would be inclined to look out for are offshore bonds as they do have a place for security and can be wrapped in a trust, and these are costly options.

In this table, I will do a brief guide on the charges of some of the funds and the platforms this will vary significantly on the amount of commission the advisor takes and fund charges. Also, note that the advisors can also add a management fee for this.

- Note that this is just a brief guide for more in-depth analysis please read some of my articles or full investments offshore guide.

My thoughts on offshore bonds

I believe they do still have a place for a small minority of people, more so looking for estate planning if for example wanting a trust or over the NRB of 325,000 GBP in the U.K.

But, if you read my article on SIPPs and IHT planning you have better options.

If you have one of these or have been proposed one gets in touch on the form below and will review the charges and performance.

Offshore platforms

More modern advisor platforms are for me a much better option for fees and give investors in the offshore market real options to the U.K advisors.

These have the option to move SIPPs into if in the U.K or a QROPs or International SIPPs if outside. As well as this you can invest as a platform, these are portable for expats.

All of these are advisor platforms, so will have to speak to an advisor which might have an attached fee for management. However, if the advisor is good, the fee shouldn’t make a blind bit of difference providing it is around the average stated above of 1.2%

Here are a few of my top advised ones and the fees this is not an in-depth review, please read more on my blogs on U.K SIPPs international platforms with ratings or get in touch to see which is the best step for you.

Platform NameFeesDealing chargesCurrency OptionsFundsCapital Platform0.4%0.2%Yes2500+Ardan International0.4%45 USDYes2000+Custodian0.7%45 USDYes5000+Investor Trust Select1%NoneYes2000+

Thoughts are that for U.K expats now they do offer good options offshore that you can take advantage of or attempt to keep an ISA in the UK. Personally, I favour the offshore market because taxes are lower with more investment options, such as Trusts and bonds etc.

The U.K tax levels

If you are to invest outside of an ISA or tax wrapper the current levels are 12,500 GBP for U.K income tax, Capital Gains tax on anything over 12,300 GBP, and dividend tax on anything over 2000 GBP. So, it is worth keeping an eye on or seeing an advisor about your options on this.

Final thoughts, for those that are living abroad I would be more inclined to look at international SIPPs, ISA limits may be put on the radar and see the amount reduced due to a money-strapped government. ISA’s are very popular with many UK citizens and does have a use, however, as an expat they can be hard to get and are likely to lose some of its tax freedoms. Furthermore, if you are living abroad, you do now have feasible offshore funds and stocks and platforms.

Summary

If you are still stuck on which is the best financial advisor for your situation, contact a few, give them the details they need, and then compare all the fees, charges, commissions, and investments they recommend.

Take what they suggest, put it into Morningstar or a similar website and then see what the investments are like. By doing this you will weed out the advisors who are after the commission and those who have your best interest at heart.

Finally, the best advisors aren’t always the ones that charge the most more often they have higher amounts for lump-sums and monthly installments. They are usually the ones with reasonable fees and a good understanding of how they can better your situation.